The Finance Ministry in a series of tweets clarified that rights of depositors will not be compromised by The Financial Resolution and Deposit Insurance Bill, 2017, or FRDI Bill, expected to be tabled in the Parliament in the upcoming winter session. The ministry said that "besides providing similar protection /guarantee of Rs.1 lakh to depositors,as it exists today, the rights of uninsured depositors are being placed at an elevated status in the FRDI Bill compared to existing legal arrangements over the unsecured creditors and even Government dues."

This clarification comes after a series of news articles and columns in the media expressing concerns over the safety of deposits in the banking system once the FRDI Bill becomes an Act and is notified by the government. That the government machinery is rattled by the voices against the bill could be gauged from the fact that finance minister Arun Jaitley was also forced to issue a clarification on Wednesday evening on Twitter.

A viral message going around on WhatsApp, apparently written by a Mumbai based CA, titled "This Tsunami will wipe out your money lying in the Banks" has also created panic among depositors. PSU bank unions are protesting the move as they have argued that several provisions in the bill are against depositors and will cause an environment of mistrust between the banks and depositors.

"If this bill is passed, the trust will be lost. The banks will be allowed to use depositors money as per their wish. As it is, we do not get adequate interest. Now they want to use our money for resolution of bad debts. As a depositor, we are squeezed from both sides. For bank employees, any loss of trust with the depositors means bad news," said Vishwas Utagi, Vice-President, All India Bank Employees Association.

In the last ten days, several messages were circulated on WhatsApp that talks about the bail-in clause in the new bill that will give more teeth to the banks and regulators to use public deposits to make good the losses suffered by way of loans that are never recovered from big borrowers.

1) But first, let us understand what are the provisions today when a bank goes bust?

In 70-years of independent India history, no PSU bank has gone bust. There are cases of several co-operative banks and private sector banks that have shut down, but the RBI has stepped-in to merge banks on the verge of a collapse with bigger banks. In 2014, public sector bank Canara Bank took over the assets of Amanath Co-operative Bank Ltd, Karnataka’s first scheduled urban co-operative bank. According to this report in the Livemint, while deposits up to Rs 1 lakh were protected under the insurance scheme, any deposits above that had to take a 18% haircut.

In 2004, Global Trust Bank went bust following high exposure to the stock market in the 2001 Ketan Parekh scam. In a bid to save one million depositors, RBI stepped in and forced the bank to merge with Oriental Bank of Commerce. While the shareholders took a hit as no share swap deal was provided for, the depositors were protected by the merger.

Also in 2004, Mumbai-based South Indian co-operative bank shut down following nexus between bank employees and politicians resulting in issuance of loans that could never be recovered. The country’s biggest co-operative bank, Saraswat Bank finally took over in 2008 and it was widely reported that depositors would have to forego some part of their unsecured deposits.

But 45-year old John Samuel whose family had multiple deposits worth Rs 10 lakhs in the bank told BOOM that all they got was Rs 3 lakhs (Rs 1 lakh insured amount for each account) under the deposit insurance scheme. The rest of the unsecured deposits never came back even after Saraswat took over the bank in 2008.

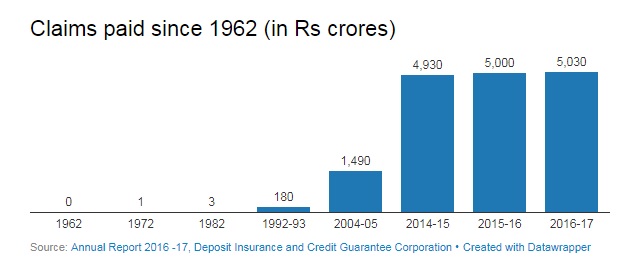

2) How much has DICGC paid to depositors by way of insurance claims?

The Deposit Insurance and Credit Guarantee Corporation has paid claims amounting to Rs 5,000 cr since 1962 when the Act came into force. The DICGC’s Deposit Insurance Fund has around Rs 80,000 crores that covers 92% of all account holders in the banking system. 30 per cent of the total deposits are insured - in line with international norms that mandate 20-30% of the deposits to be insured. According to DICGC’s annual report of 2016-17, 2125 banks are covered by their scheme.

Sources at DICGC point out that 90% of the total insurance claims have come from depositors of co-operative banks since inception.

3) So, why FRDI Bill?

Contrary to popular perception, the FRDI Bill is not an invention of the Narendra Modi government. India is part of the Group of 20 economies (G20) group that have endorsed The Financial Stability Board’s proposal called ‘Key Attributes of Effective Resolution Regimes for Financial Institutions’. This proposal has a provision for ‘bail-in’ to ensure that a country’s economy is not destabilised in the event of a big default by a large bank(s).

The Financial Stability Board was set up in 2009 post the global financial crisis in 2008 when US had to bail out big banks with taxpayer money to prevent a large scale systemic collapse. The learnings from this catastrophic event for central bankers was to never reach a similar situation where governments have to dip into taxpayers money to bail out banks or allow any institution to become 'too big to fail'.

The FRDI Bill thus aims to operationalise the setting up of a Resolution Corporation that would help stabilise financial institutions in an orderly manner without taxpayer exposure to loss from solvency support, while ensuring key areas of operations do not suffer.

4) But what about depositors? What has changed for them?

Given below is the text of the preamble taken from the Financial Stability Board's website.

"The objective of an effective resolution regime is to make feasible the resolution of financial institutions without severe systemic disruption and without exposing taxpayers to loss, while protecting vital economic functions through mechanisms which make it possible for shareholders and unsecured and uninsured creditors to absorb losses in a manner that respects the hierarchy of claims in liquidation."

Here is where the concept of the bail-in comes into force through section 52 of the FRDI Bill. A bail-in is opposite of a bail-out and ensures that in the event of a financial institution's collapse, the creditors and depositors will have to absorb some of the losses.

"....the Corporation may, in consultation with the appropriate regulator, if it is satisfied that it necessary to bail-in a specified service provider to absorb the losses incurred, or reasonably expected to be incurred, by the specified service provider and to provide a measure of capital so as to enable it to carry on business for a reasonable period and maintain market confidence, take an action under this section by a bail-in instrument or a scheme to be made under section 48...."

The Bill however makes it clear that the bail-in clause will not apply to the insured deposits and several other categories.

"The bail-in instrument or scheme under this section shall not affect—(a) any liability owed by a specified service provider to the depositors to the extent such deposits are covered by deposit insurance;

(b) any liability that the specified service provider has by virtue of holding client assets."

To make it clear, from a depositor's point of view, the risk profile has not changed substantially as it exists today. Post the notification of the Act, a bail-in clause will not apply to the deposits covered by insurance. The Bill is however silent on the upper limit of deposit insurance with divergent views among banking industry experts if the limit of Rs 1 lakh per account will be maintained or whether it will be increased. However most industry watchers are unanimous in their view that there is very little chance the government will reduce the present insurance cover of Rs 1 lakh.

Considering that the depositors are looking at the bail-in clause with suspicion, the finance ministry has also clarified that the legal provisions in the bill will ensure that the rights of the depositors are considered at an elevated level over unsecured creditors and dues owed to the government.

While it is too early to give a clean-chit to the bail-in provisions, banking experts argue that it will be politically suicidal for any government to hurt the interests of depositors, unless in extreme cases where the country's economic ecosystem is on the verge of a collapse.

"If depositors lose confidence in the banking system, it will be a big systemic loss and difficult to regain that trust. It will be a very cold day in May before any regulator will allow the interests of ordinary depositors to be compromised, " said Harsh Roongta, a former banker and SEBI registered investment advisor.

5) When can the Resolution Corporation go for liquidation of a bank and how are unsecured deposits protected?

According to the Bill, the Corporation, in consultation with the respective regulators (e.g. RBI for banks, and IRDA for insurance companies) will specify criteria for classifying service providers based on their risk of failure. The 5 categories are "Low, Moderate, Material, Imminent and Critical".

Out of these five categories, the threat to a depositor's unsecured deposits only comes in when a institution is categorised as 'critical'. The Corporation will undertake its resolution by using options which include: (i) transfer of its assets and liabilities to another person, (ii) merger or acquisition, and (iii) liquidation, among others.

Proceeds from the sale of assets will be distributed in the following order:

- Amount paid by Corporation as deposit insurance to insured depositors

- Resolution costs

- Workmen dues for 24 months and secured creditors

- Wages owed to employees other than workmen for the period of twelve months preceding the date of the commencement of liquidation commencement date

- Amount to uninsured depositors and other insurance related amounts

- Unsecured creditors

- Government dues and remaining secured creditors

- Remaining debt and dues, and

- Shareholders.

While in the case of South Indian co-operative bank in 2008, depositors have complained that they did not receive any of their deposits beyond the insured Rs 1 lakh, the FRDI Act has clearly laid out procedures on how the proceeds from the sale of assets should be distributed. Though unsecured deposits will have to take a haircut if the sale of assets are not enough to meet all categories of claims, the remaining amount will be disbursed proportionately within each class of claims as mentioned above.

6) Key Concerns

Despite the entry of several private banks in the country in the last 25 years, a public sector bank is still seen as a highly safe avenue to park your deposits. This is one reason why depositors, especially senior citizens park their savings in PSU banks despite a low interest regime in recent years and better avenues of investment like mutual funds.

But a bail-in option implicitly holds a depositor who provides low-cost capital to the bank to lend to others, responsible for the losses of the bank along with other unsecured creditors. Also the failure of the bill to quantify the deposits that will come under the insurance scheme has also led to worries among depositors if their interests will actually be protected.

The government recently provided Rs 2 lakh crore by way of recapitalisation of PSU banks. Total bad loans of the country's 38 listed commercial banks have touched the Rs 10 lakh crore figure at the end of September quarter this year. This amounts to over 12 per cent of the total loans given by the banking industry.

But here is the catch. PSU banks have over 90 per cent of these non-performing assets on their books. The government has already made its intention clear to consolidate loss making banks with bigger banks in order to improve the financial health of these entities.

Unless these moves are matched by a tight rap on the knuckles of wilful defaulters and accountability of bankers who manage the disbursal of loans made under questionable circumstances, the bail-in clause will always be looked at with suspicion as a case of "robbing Peter to pay Paul".